FlexShopper made lease-to-own shopping accessible for people with limited credit, and in 2026 the buy now pay later and installment payment ecosystem has expanded dramatically with alternatives offering 0% interest, credit-building features, and universal merchant acceptance. Whether you need interest-free installments at your favorite stores, lease-to-own financing for furniture and electronics, or service financing for dental work and auto repairs, there is an app designed for your specific needs.

This guide reviews 12 apps like FlexShopper covering traditional Pay in 4 platforms, lease-to-own alternatives, credit-building installment apps, and service-specific financing. We evaluate each app on flexibility, interest rates, credit impact, merchant network, and approval accessibility. For related financial tools, check our guides on budgeting apps, investment apps, and digital planners for managing your finances.

Table of Contents

- Klarna (Rating 4.8)

- Affirm (Rating 4.8)

- Afterpay (Rating 4.8)

- Zip (Rating 4.8)

- Fingerhut (Rating 4.7)

- Sezzle (Rating 4.5)

- Katapult (Rating 4.5)

- FlexShopper (Rating 4.5)

- PayPal Pay in 4 (Rating 4.2)

- Perpay (Rating 4.0)

- Splitit (Rating 4.0)

- Sunbit (Rating 3.9)

- Which App Is Right for You?

- Tips for Using BNPL Apps Responsibly

- Frequently Asked Questions

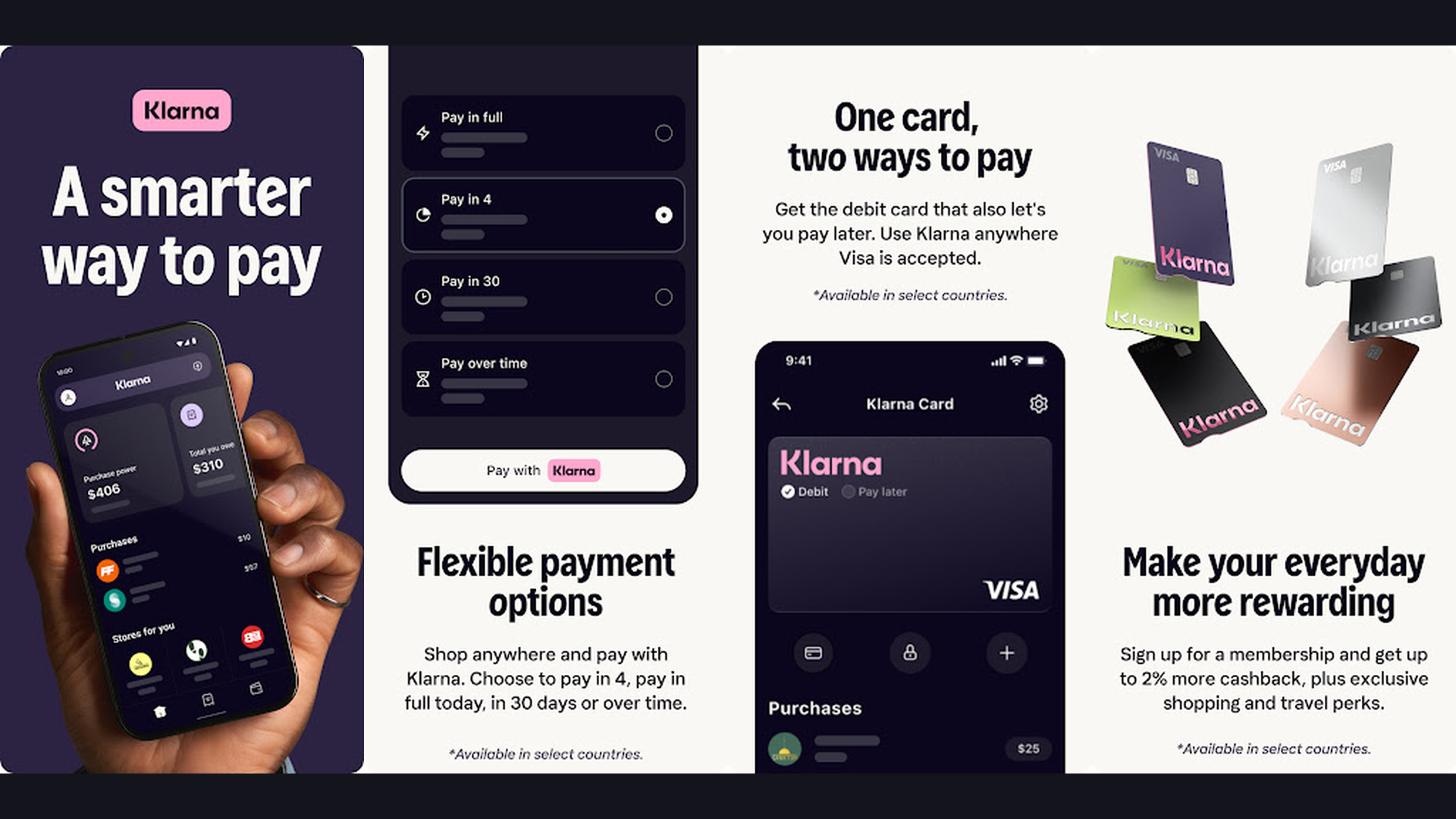

1. Klarna (Rating 4.8)

Klarna is a global BNPL leader with over 150 million users offering Pay in 4, Pay in 30 Days, and monthly financing with no hard credit check. The Pay in 4 option splits any purchase into four interest-free installments every two weeks, making it the most flexible mainstream alternative to FlexShopper. Klarna only performs soft credit checks that do not affect your credit score. The Klarna app includes a full shopping browser with exclusive deals, price drop alerts, and cashback at partner retailers. The one-time virtual card feature lets you use Klarna at any online store, not just partner merchants. The Klarna Card extends buy-now-pay-later functionality to in-store purchases anywhere Visa is accepted. Klarna Checkout integrates with over 500,000 retailers globally. The Wish List feature tracks prices and notifies you of drops. The CO2 tracker shows the environmental impact of your deliveries. Klarna is free with 0% APR on Pay in 4. Monthly financing ranges from 0-24.99% APR depending on creditworthiness. For shoppers who want the most versatile BNPL platform with the widest retailer network, Klarna offers more payment flexibility than FlexShopper. Track your payments with budgeting apps.

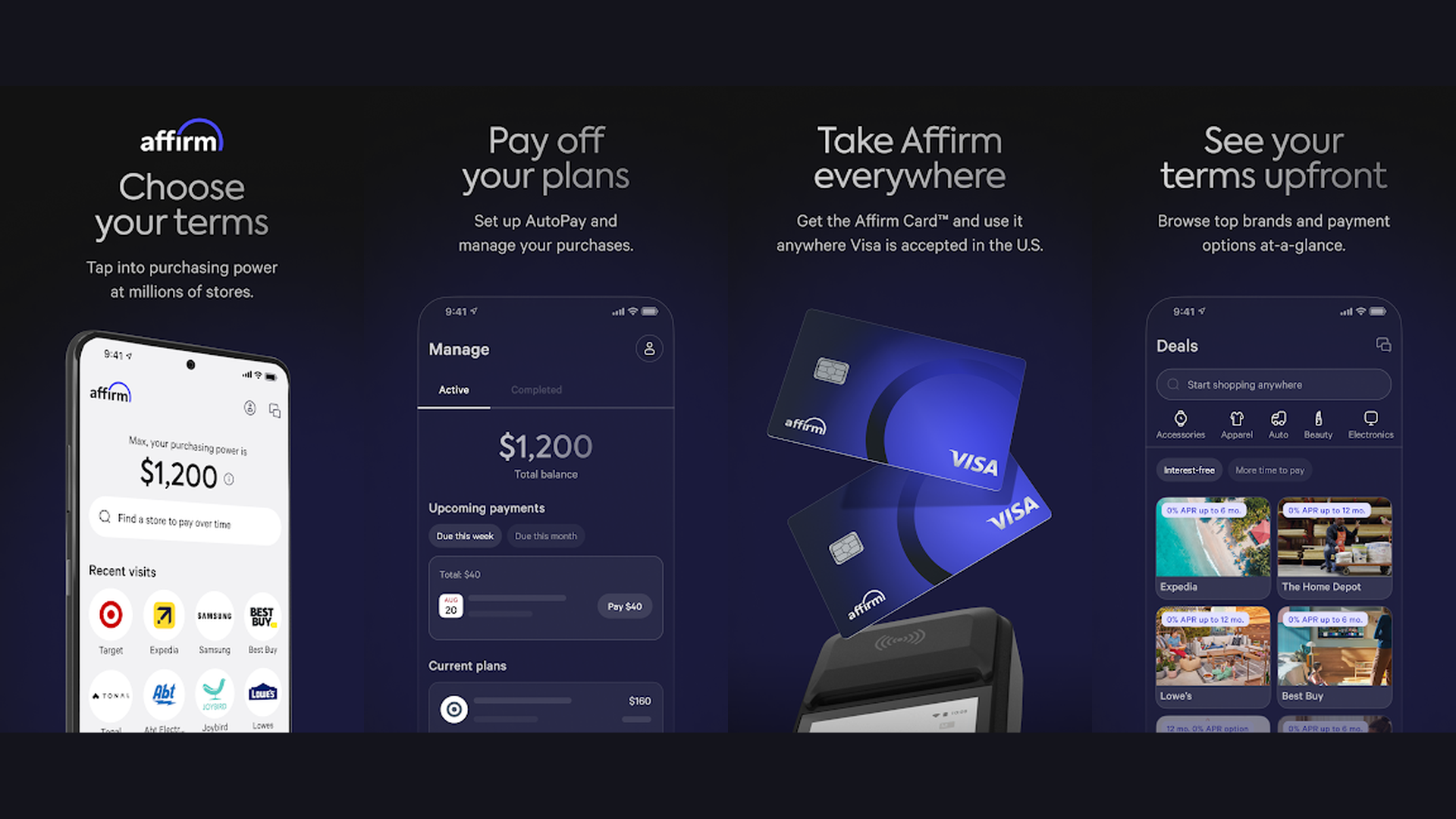

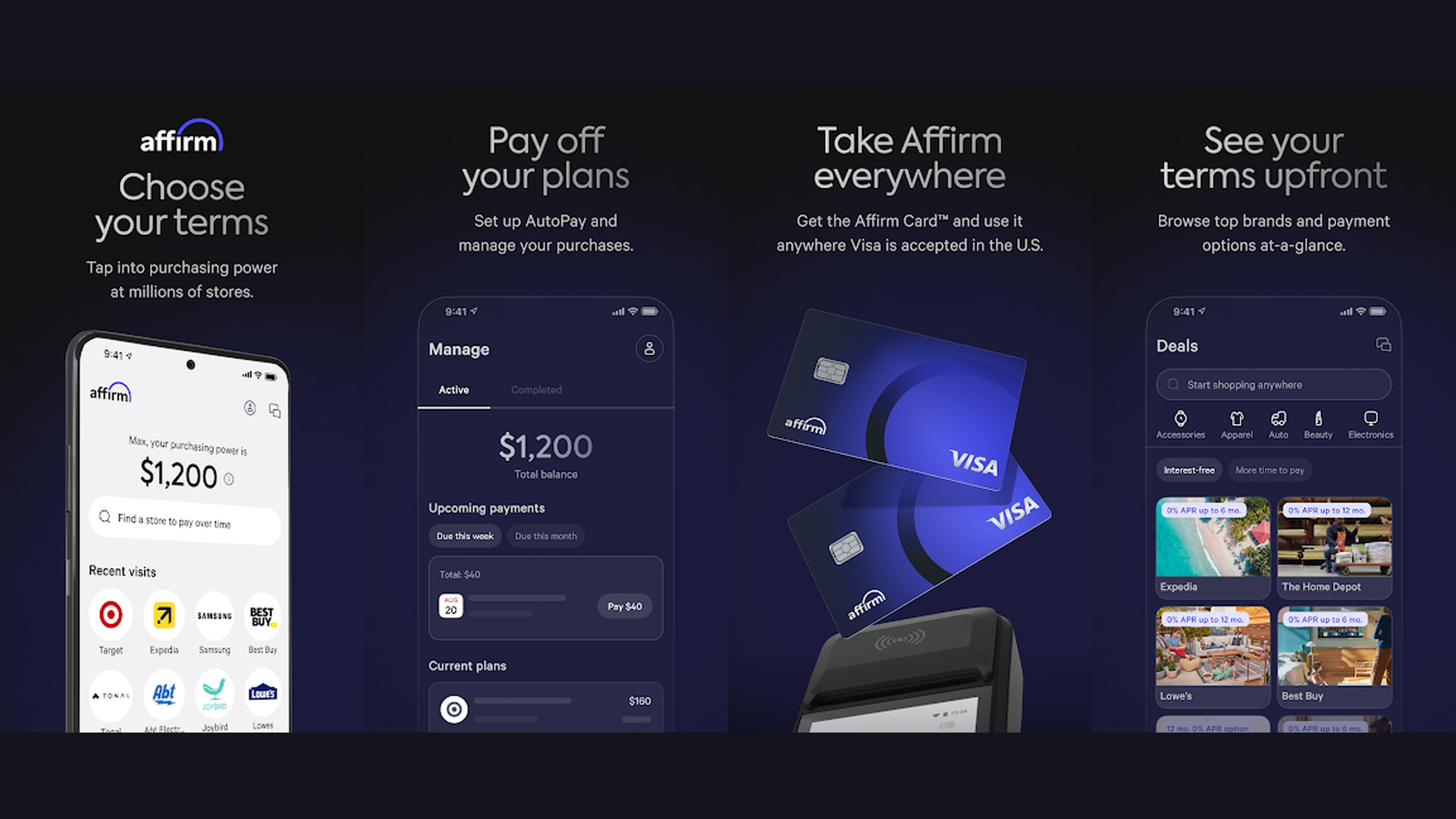

2. Affirm (Rating 4.8)

Affirm is a transparent installment payment platform offering 0% APR options for Pay in 4 and longer-term financing up to 60 months with no hidden fees. What separates Affirm from FlexShopper is absolute pricing transparency: you see the total cost upfront before committing, and Affirm never charges late fees, prepayment penalties, or hidden service charges. The Pay in 4 option provides four biweekly interest-free payments for smaller purchases. For larger purchases, Affirm offers monthly plans from 3 to 60 months with APRs ranging from 0% to 36% based on your credit profile. Affirm partners with over 300,000 retailers including Amazon, Walmart, Target, and Best Buy. The Affirm virtual card works anywhere Visa is accepted for one-time purchases. Affirm now reports payment history to credit bureaus, helping you build credit with on-time payments. The Affirm app features deal alerts and exclusive offers from partner merchants. Affirm is free to use with 0% APR options available. For shoppers who want honest, transparent installment plans with no surprise fees and potential credit-building benefits, Affirm is the most transparent BNPL option.

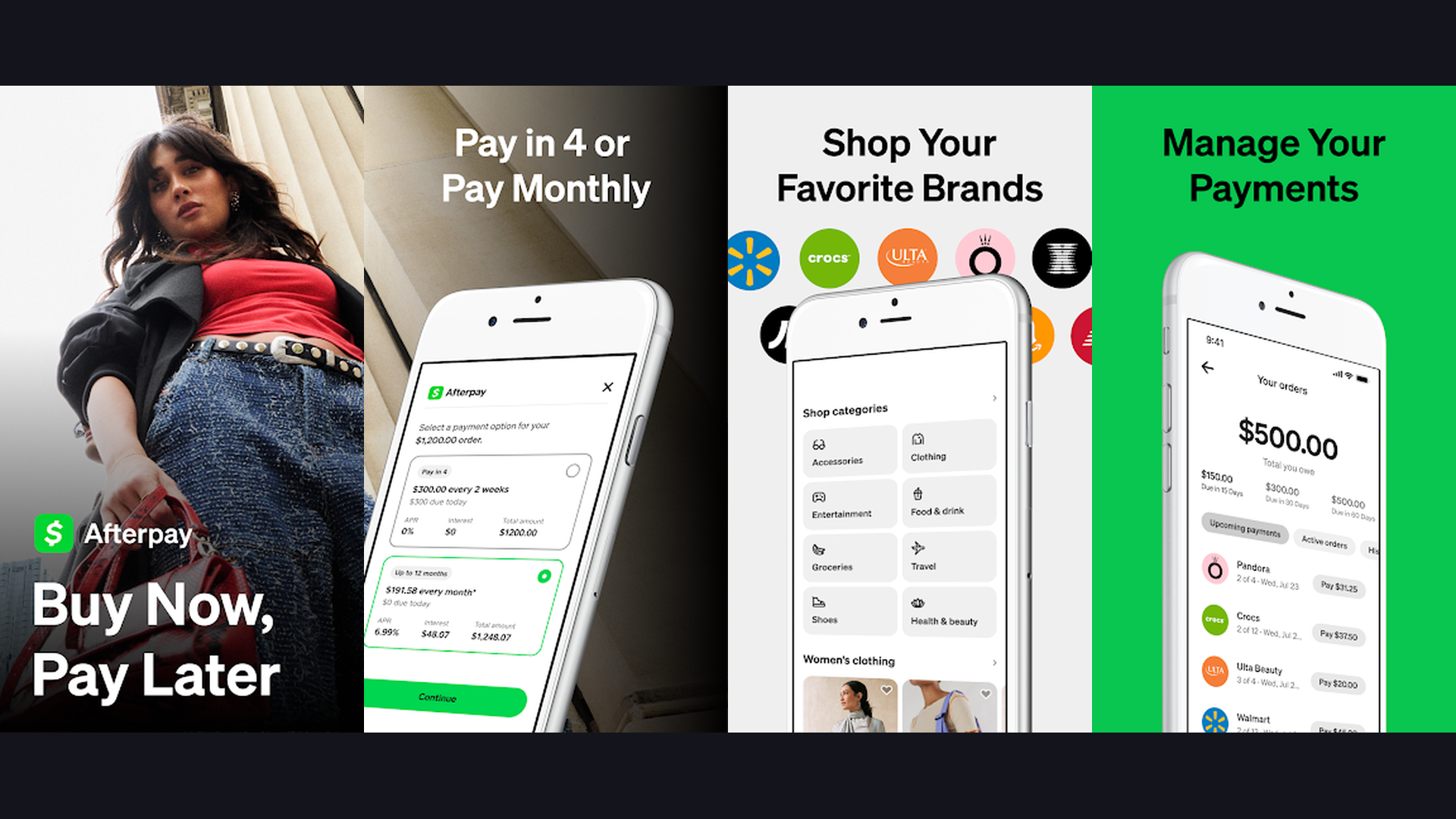

3. Afterpay (Rating 4.8)

Afterpay is a pioneer of the Pay in 4 model with seamless in-store and online shopping at over 100,000 retailers with no interest charges. Afterpay splits every purchase into four equal payments due every two weeks with 0% interest, no credit check for standard purchases, and no annual fees. The in-store Afterpay Card (powered by Visa) lets you tap to pay at physical retail locations and automatically split the transaction into four payments. The app features curated shopping categories, trending deals, and exclusive Afterpay Day sales events. The Afterpay Pulse Rewards program gives perks and benefits for responsible payment behavior, including the ability to increase spending limits and unlock exclusive offers. Afterpay partners with major brands including Nike, Sephora, Urban Outfitters, ASOS, and Adidas. The Cash App integration (Afterpay is owned by Block/Square) enables direct payment management. Afterpay is completely free with 0% interest on all Pay in 4 purchases. Late fees apply for missed payments (capped at 25% of the order value). For fashion and lifestyle shoppers who want zero-interest installments at trendy retailers, Afterpay dominates the lifestyle BNPL space.

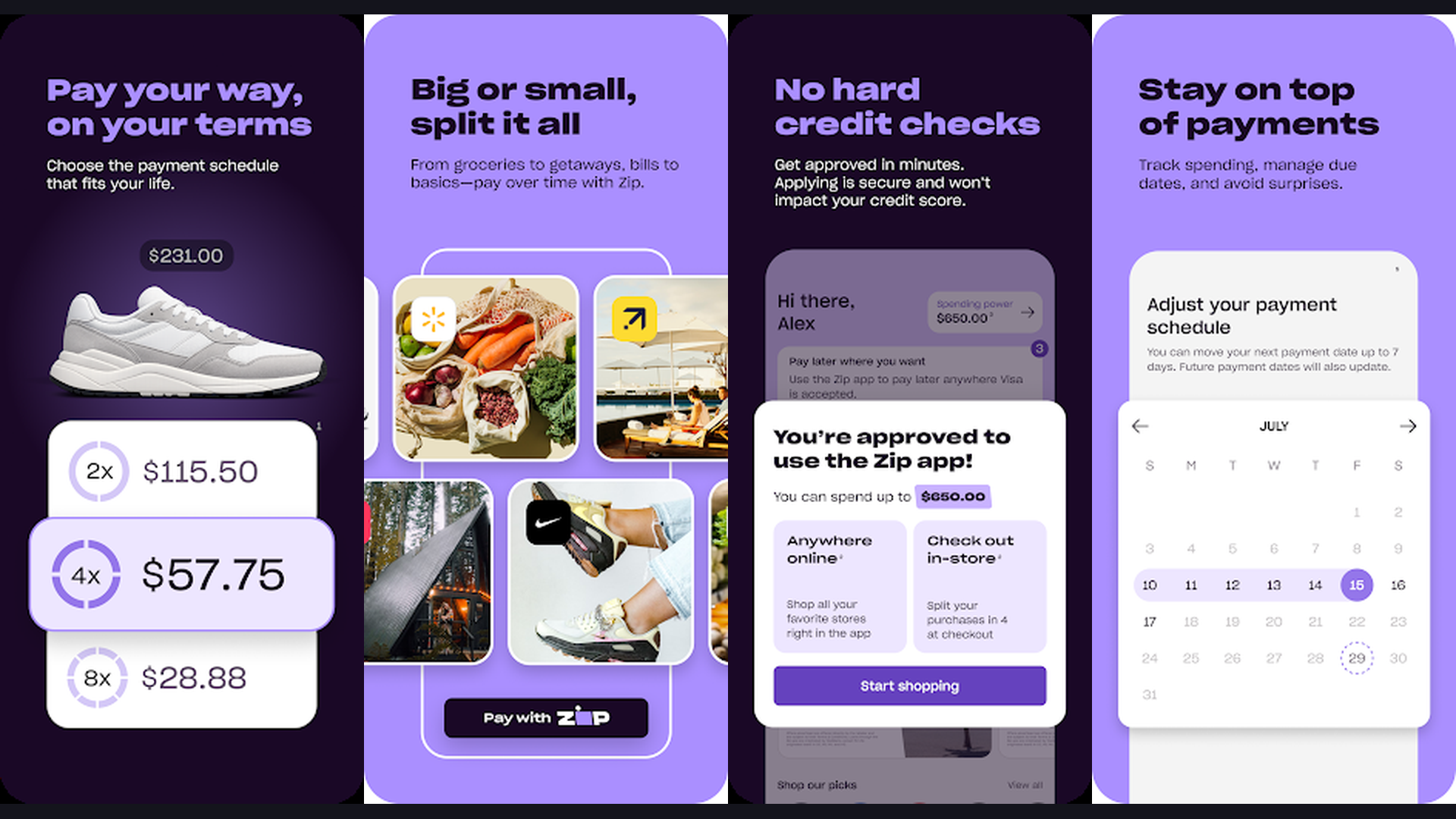

4. Zip (Rating 4.8)

Zip (formerly Quadpay) is a virtual card BNPL platform that works anywhere Visa is accepted, not just at partner merchants, giving you FlexShopper-like flexibility with pay-in-4 simplicity. This is the key advantage over other BNPL apps: Zip generates a one-time virtual Visa card that you can use at literally any online or in-store retailer. You are not limited to a network of partner merchants. Split any purchase into four biweekly interest-free payments. The Zip app also integrates with Apple Pay and Google Pay for contactless in-store payments. The Shop section features curated deals and cashback offers at partner retailers. Zip Rewards gives you points on every purchase redeemable for gift cards and discounts. The spending tracker helps you monitor all your installment obligations in one place. Zip performs only soft credit checks. Zip is free with 0% interest on standard Pay in 4. A $1 installment fee may apply on some transactions. For shoppers who want to use BNPL anywhere Visa is accepted without merchant restrictions, Zip delivers the most universal payment flexibility.

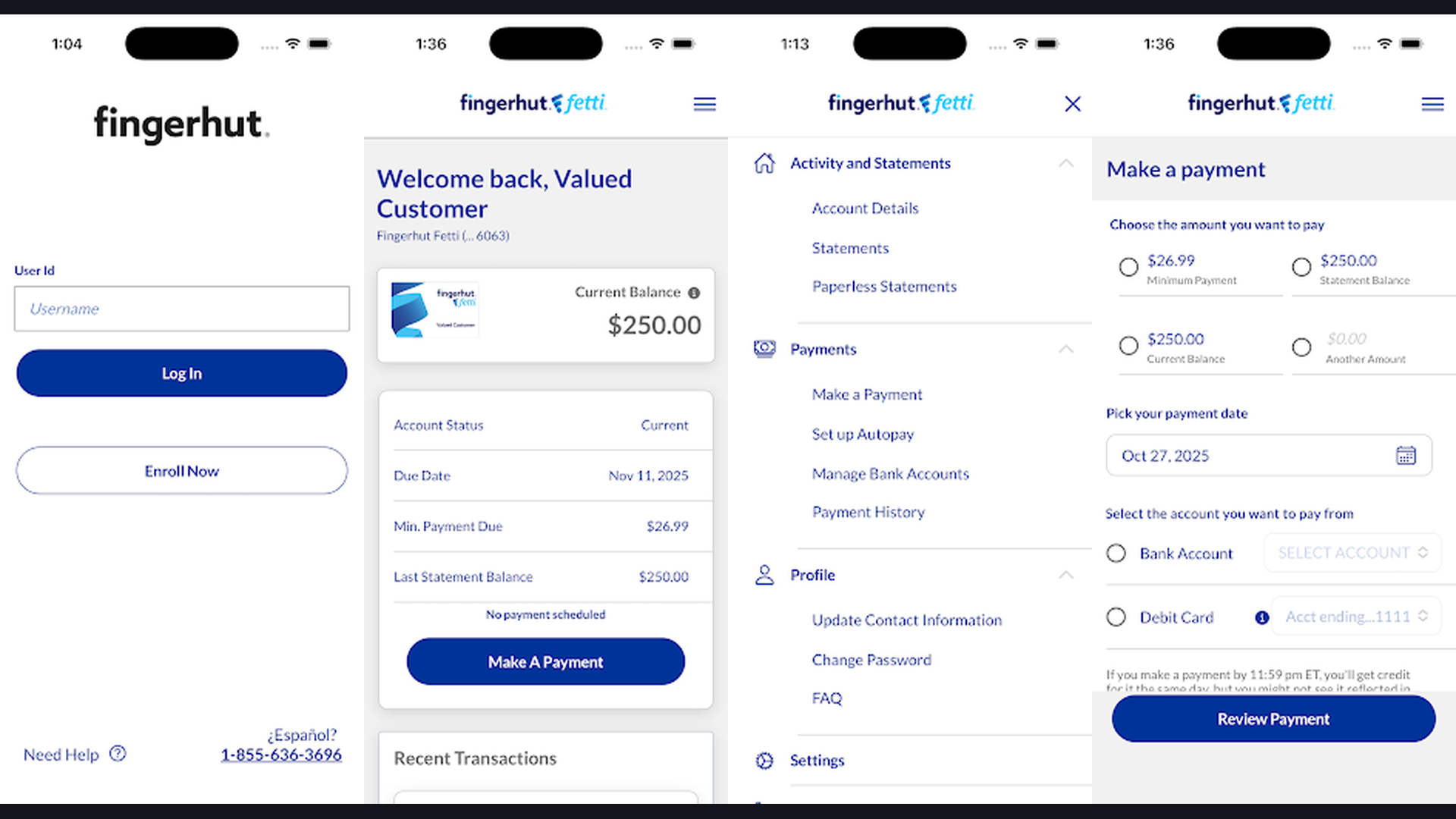

5. Fingerhut (Rating 4.7)

Fingerhut is a credit-building online retailer offering a revolving credit account with low monthly payments on electronics, furniture, appliances, and thousands of products. Unlike standard BNPL apps, Fingerhut provides a revolving WebBank credit account specifically designed for people with limited, fair, or bad credit who may not qualify for FlexShopper or traditional financing. Fingerhut reports monthly payments to all three major credit bureaus (Experian, TransUnion, Equifax), making it one of the most effective credit-building tools disguised as a shopping platform. The product catalog includes over 100,000 items across electronics, home goods, clothing, furniture, appliances, and more from recognized brands. Monthly payments are spread over manageable terms. The Fingerhut Fresh Start program helps first-time credit builders establish a history. The app features exclusive sales, order tracking, and payment management. Fingerhut charges APR of 29.99% on the revolving credit line. For shoppers focused on building or rebuilding credit while purchasing everyday items with manageable payments, Fingerhut is the strongest credit-building alternative to FlexShopper. Great alongside investment tools.

6. Sezzle (Rating 4.5)

Sezzle is a BNPL platform with an optional credit-building feature (Sezzle Up) that splits purchases into four interest-free payments over six weeks. The unique Sezzle Up program is what distinguishes Sezzle from other Pay in 4 apps: opt in, and Sezzle reports your on-time payment history to credit bureaus to help you build credit. This makes Sezzle one of the few BNPL apps that actively helps improve your credit score. The standard Pay in 4 splits purchases into four biweekly payments with 0% interest. Sezzle performs only soft credit checks. The payment schedule gives you six weeks to pay instead of the standard eight, meaning faster payoff. The Sezzle Virtual Card works at any online retailer, expanding beyond partner merchants. Sezzle partners with over 47,000 retailers including popular fashion, beauty, and lifestyle brands. The reschedule feature lets you push back a payment once for free if you need extra time. Sezzle is free with 0% interest on Pay in 4. Sezzle Premium ($4.99/month) unlocks unlimited reschedules and higher spending limits. For shoppers who want interest-free installments plus credit-building benefits, Sezzle offers the best combination.

7. Katapult (Rating 4.5)

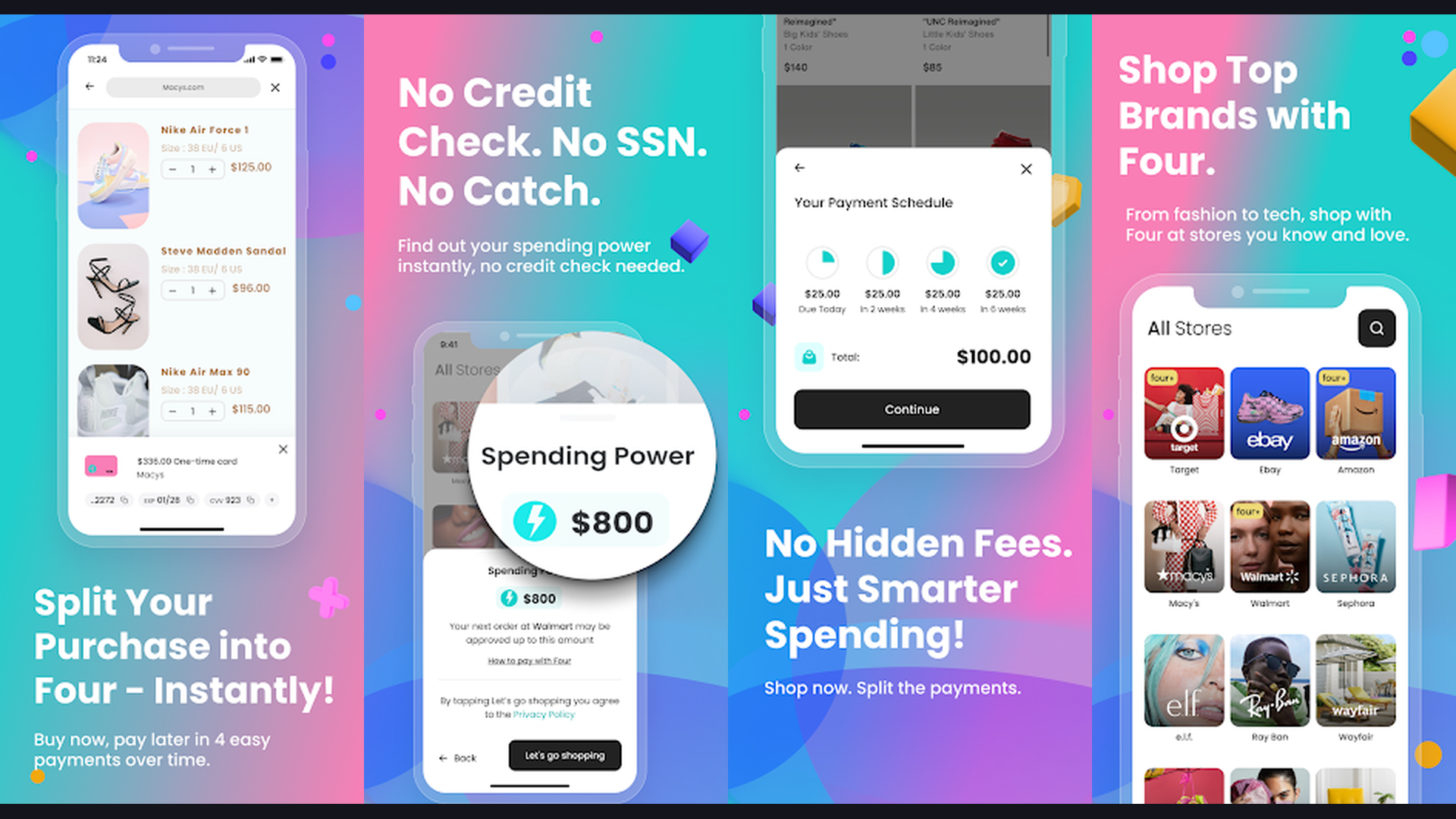

Katapult is a lease-to-own platform with no credit check that is the closest direct alternative to FlexShopper for furniture, electronics, and appliances. Like FlexShopper, Katapult uses a lease-to-own model rather than traditional credit, making it accessible to shoppers with poor or no credit history. Apply online and get an instant decision without a hard credit inquiry. Shop at hundreds of partner retailers including Wayfair, Lenovo, Purple, Dyson, Samsung, and furniture stores. The flexible payment schedule lets you pay weekly, biweekly, or monthly. The early buyout option saves you money: pay off your lease in 90 days and pay close to the retail price. After 90 days, the total cost increases. The app tracks all your leases, payment schedules, and early buyout options in one dashboard. Katapult spending limits typically range from $500 to $3,500 based on your financial profile. Katapult is free to apply with no hard credit check. The total lease cost is typically 1.5-2x the retail price if paid over the full term. For shoppers with limited credit who need furniture, electronics, or appliances, Katapult is the most direct FlexShopper competitor.

8. FlexShopper (Rating 4.5)

FlexShopper is the original lease-to-own marketplace offering flexible weekly payments on electronics, furniture, appliances, and more with no traditional credit check. FlexShopper uses a proprietary underwriting algorithm that considers factors beyond your credit score, making approval possible for shoppers who get declined elsewhere. Shop from FlexShopper direct marketplace or use the FlexShopper virtual card at participating retailers. Spending limits typically range from $500 to $2,500. Weekly payment plans spread the cost over 52 weeks, making individual payments manageable. The 90-day purchase option lets you own the item at a significant discount by paying off within the first 90 days. The FlexShopper marketplace features thousands of products across electronics, furniture, tires, appliances, gaming consoles, and home goods. Order tracking and payment management are handled through the app and online portal. FlexShopper charges a lease-to-own fee that typically results in a total cost of 1.5-2x the retail price over the full 52-week term. For shoppers who need immediate access to essential items with no credit requirements, FlexShopper pioneered the lease-to-own marketplace concept. Manage payments alongside digital planners.

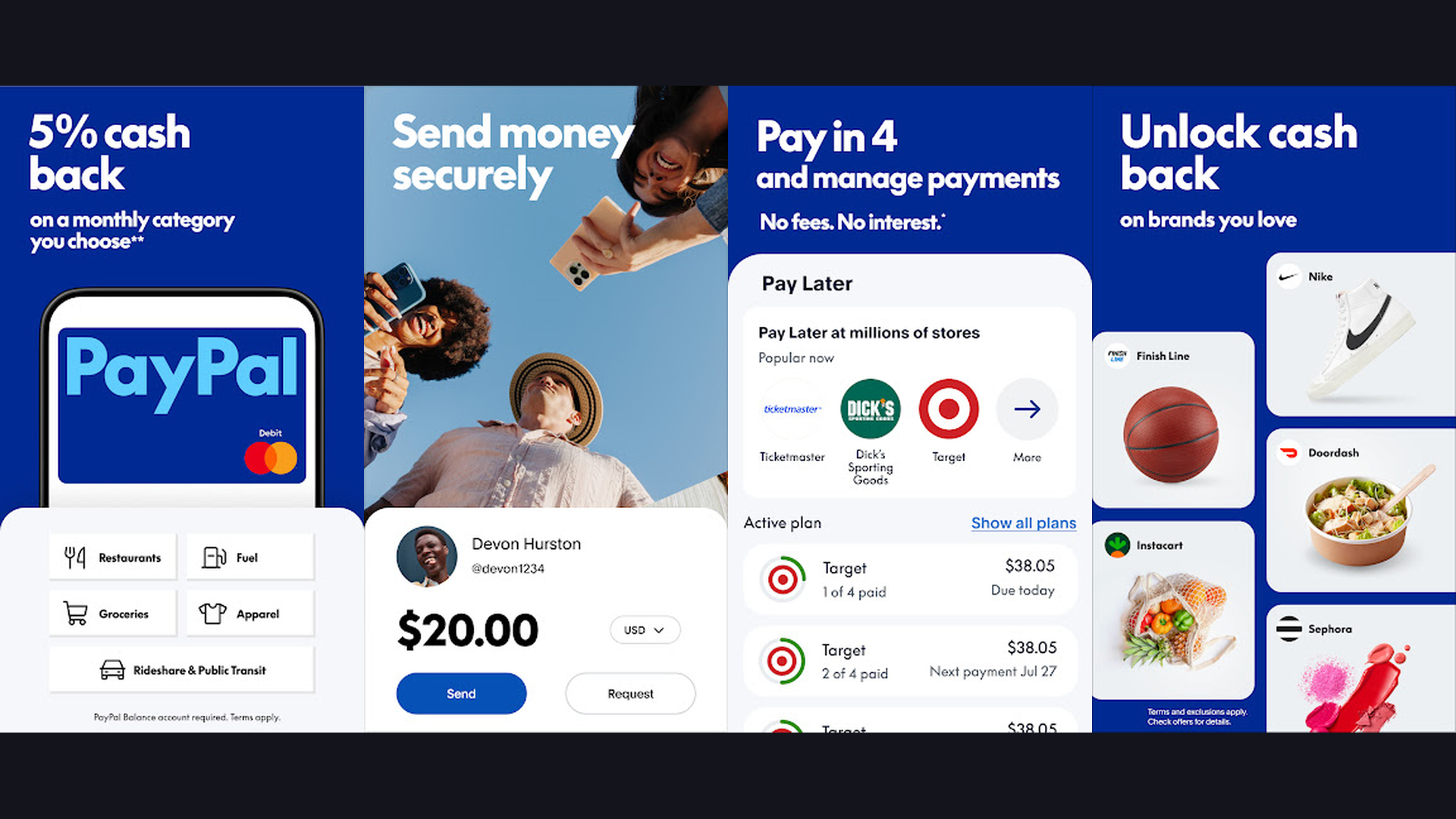

9. PayPal Pay in 4 (Rating 4.2)

PayPal Pay in 4 is a built-in BNPL feature within the PayPal app that splits purchases between $30 and $1,500 into four interest-free biweekly payments with PayPal buyer protection. The biggest advantage of PayPal Pay in 4 over dedicated BNPL apps is that it works within PayPal, which already has over 430 million active accounts and is accepted at millions of merchants worldwide. No new app to download, no new account to create. Simply select Pay in 4 at checkout wherever PayPal is accepted. PayPal performs a soft credit check that does not affect your score. All purchases are protected by PayPal Buyer Protection, covering you if items do not arrive or do not match the description. The seamless integration means your existing PayPal balance, linked bank accounts, and cards can all fund the payments. The PayPal app dashboard tracks all your installment plans alongside your regular PayPal activity. PayPal Pay in 4 is completely free with 0% interest and no fees. Late fees of up to $10 may apply for missed payments. For existing PayPal users who want hassle-free installment payments without signing up for another service, Pay in 4 is the easiest BNPL entry point. Check our wellness guide for healthy shopping habits.

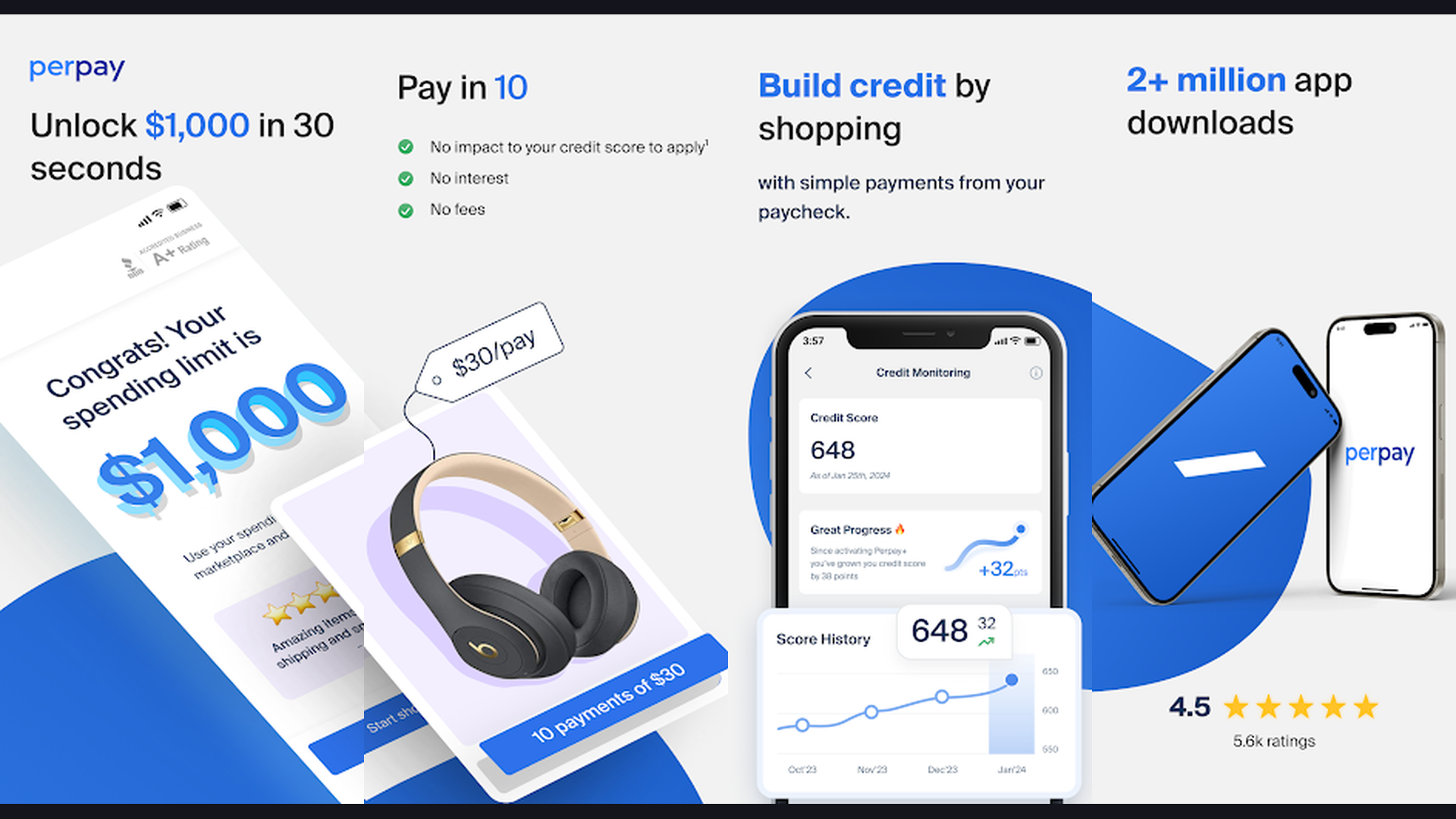

10. Perpay (Rating 4.0)

Perpay is a paycheck-linked shopping platform with no credit check, no interest, and automatic credit reporting to help you build your credit score. Perpay takes a completely different approach to flexible payments: instead of splitting a purchase into four installments on a set schedule, Perpay deducts payments directly from your paycheck via employer payroll integration. This automatic deduction eliminates the risk of missed payments and helps build a consistent payment history. Perpay reports all on-time payments to Experian and TransUnion, actively building your credit with every purchase. The product catalog includes electronics, home goods, fashion, beauty, appliances, and more from recognized brands. No credit check is required to apply. Approval is based on your employment income rather than credit history. The Perpay Marketplace features deals and promotions exclusive to the platform. Average payment terms range from 3 to 12 months depending on the purchase amount. Perpay charges no interest and no fees. Prices on some items may be marked up compared to retail. For employed shoppers who want automatic payments from their paycheck with guaranteed credit building, Perpay eliminates the discipline needed to manage manual installments.

11. Splitit (Rating 4.0)

Splitit is a unique installment platform that uses your existing credit card to split payments into 2-12 monthly installments with no additional interest, fees, or credit checks. Splitit operates fundamentally differently from FlexShopper and other BNPL apps: rather than creating a new line of credit or lease, Splitit simply divides your existing credit card charge into equal monthly installments. Your credit card issuer holds the full purchase amount, and Splitit releases it in installments. This means no new credit application, no additional interest beyond what your credit card charges, no late fees from Splitit, and no effect on your credit score. The major advantage is that you continue earning your credit card rewards points and cashback on the full purchase. Splitit works with Visa and Mastercard at participating merchants. Payment terms range from 2 to 12 months. Splitit is completely free with zero fees. You pay only any interest your credit card normally charges. For shoppers who already have a credit card and want to spread payments while earning credit card rewards, Splitit adds installment flexibility to your existing card without any additional cost.

12. Sunbit (Rating 3.9)

Sunbit is a point-of-sale financing platform specializing in essential services like dental care, auto repair, eye care, and veterinary bills with a 90% approval rate. While FlexShopper focuses on product purchases, Sunbit fills a critical gap by financing services that most BNPL apps do not cover. Need dental work, new tires, car maintenance, or pet surgery? Sunbit offers financing at the service provider checkout with a 30-second application and instant decision. The 90% approval rate makes it one of the most accessible financing options in the market. Sunbit performs only a soft credit check. Payment plans range from 3 to 72 months with APRs from 0% to 35.99% depending on creditworthiness. Over 20,000 service provider locations accept Sunbit across the United States. The Sunbit Card extends financing to new categories of service providers. The app manages all your payment plans, due dates, and payment history. Sunbit is free to apply with no hard credit check. For people who need to finance essential services like dental work, auto repairs, and veterinary care rather than retail products, Sunbit fills a niche that FlexShopper and other BNPL apps do not cover. Use navigation apps to find nearby providers.

Which App Is Right for You?

Best for Zero-Interest Installments (Pay in 4)

- Afterpay - Fashion and lifestyle focused, 100,000+ retailers, Pulse Rewards

- Klarna - Most versatile, 500,000+ retailers, virtual card for any store

- Zip - Works anywhere Visa is accepted, not just partner stores

- PayPal Pay in 4 - Already have PayPal? Easiest setup, buyer protection

Best for Credit Building

- Sezzle (Sezzle Up) - Optional credit reporting with interest-free payments

- Perpay - Paycheck-linked, reports to Experian and TransUnion

- Fingerhut - Revolving credit account, reports to all 3 bureaus

- Affirm - Now reports payment history to credit bureaus

Best Lease-to-Own (Direct FlexShopper Alternatives)

- FlexShopper - The original lease-to-own marketplace

- Katapult - No credit check, 90-day early buyout option

Best for Services (Not Products)

- Sunbit - Dental, auto repair, eye care, vet bills, 90% approval

Best for Existing Credit Card Holders

- Splitit - Uses your existing card, zero fees, keep earning rewards

Tips for Using BNPL Apps Responsibly

- Never Use BNPL for Impulse Purchases - The ease of splitting payments can encourage spending on items you do not need. Before using any buy now pay later app, ask yourself: would you buy this item if you had to pay the full price today? If not, the installment plan is masking an unaffordable purchase. BNPL should make planned purchases more manageable, not enable impulse buying.

- Track All Your Active Installments - It is easy to lose track when you have Pay in 4 plans running on Afterpay, Klarna, and Zip simultaneously. Use a digital planner or spreadsheet to track every active installment: the remaining balance, next payment date, and total outstanding obligations. Add up all your biweekly BNPL payments to see the true impact on your budget.

- Choose 0% Interest Options Whenever Possible - Afterpay, Klarna Pay in 4, Zip, Sezzle, and PayPal Pay in 4 all offer genuine 0% interest on short-term installments. Save the interest-bearing options (Affirm monthly plans, Fingerhut credit, FlexShopper leases) for purchases where the interest cost is justified by the necessity of the item and your inability to pay upfront.

- Use Lease-to-Own Only for Essentials - FlexShopper and Katapult lease-to-own plans can cost 1.5-2x the retail price over the full term. Reserve these for essential items (appliances, work equipment) that you genuinely need now and cannot wait for. For non-essential purchases, save up and buy outright to avoid the premium.

- Pay Off Early When Possible - Both FlexShopper and Katapult offer 90-day early buyout options at near-retail pricing. If you use lease-to-own, prioritize paying off within 90 days to minimize the total cost. Similarly, Affirm charges no prepayment penalties, so paying off early always saves money on interest-bearing plans.

- Leverage Credit-Building Features - If your credit needs work, use Sezzle Up, Perpay, Fingerhut, or Affirm to actively build your credit score. On-time installment payments reported to credit bureaus can meaningfully improve your score over 3-6 months. Once your credit improves, you qualify for better financing terms and traditional credit cards with rewards.

- Never Stack Multiple Lease-to-Own Agreements - Running multiple FlexShopper or Katapult leases simultaneously creates a dangerous financial burden. Each lease demands weekly or biweekly payments, and stacking several can consume a large portion of your income. Finish one lease-to-own agreement before starting another.

- Read the Late Fee Policies - Late fees vary dramatically: Afterpay caps them at 25% of order value, Klarna charges up to $7 per missed payment, and PayPal charges up to $10. Some apps (Affirm, Splitit) charge zero late fees. Understanding the penalty structure helps you prioritize payments if cash is tight. Manage everything with budgeting apps.

Frequently Asked Questions

What is the difference between BNPL and lease-to-own?

Buy now pay later (BNPL) apps like Afterpay, Klarna, and Affirm split a purchase into installments that you own immediately upon purchase. Lease-to-own apps like FlexShopper and Katapult give you possession of an item while you make lease payments, but you do not own it until the final payment. Lease-to-own typically costs 50-100% more than retail over the full term but requires no credit check, making it accessible to more shoppers.

Which app is best for bad credit?

For bad or no credit, FlexShopper and Katapult offer lease-to-own with no traditional credit check. Perpay requires only proof of employment. Sezzle and Afterpay perform soft checks and approve many applicants regardless of credit history. Fingerhut specifically designs its credit account for people building or rebuilding credit. Avoid apps requiring hard credit inquiries if your score is below 580.

Do BNPL apps affect your credit score?

Most BNPL apps (Afterpay, Klarna Pay in 4, Zip, PayPal Pay in 4) perform only soft credit checks that do not affect your score. However, Affirm now reports payment history to credit bureaus, which can help or hurt your score depending on payment behavior. Sezzle Up and Perpay actively report to build credit. Fingerhut reports to all three bureaus. Missed payments on any platform can potentially be sent to collections, which will damage your credit.

Are there any truly free BNPL apps?

Yes. Afterpay, Klarna Pay in 4, PayPal Pay in 4, Sezzle, and Zip all offer 0% interest with no upfront fees on their standard pay-in-4 plans. Splitit charges zero fees and uses your existing credit card. The catch is late fees: miss a payment and you will be charged. Affirm offers 0% APR on select merchants but may charge interest on longer-term plans. Truly free means no interest and on-time payments.

Which app has the highest spending limit?

For BNPL, Affirm offers financing up to $17,500 at some merchants. Klarna monthly financing can cover large purchases depending on approval. Splitit has no set limit since it uses your existing credit card balance. For lease-to-own, Katapult offers up to $3,500 and FlexShopper up to $2,500. PayPal Pay in 4 caps at $1,500. Standards Pay in 4 limits on Afterpay and Zip start lower but increase with responsible payment history.

Can I use multiple BNPL apps at the same time?

Yes, but do so carefully. Each BNPL app operates independently, so they do not see your obligations on other platforms. This creates the risk of overcommitting financially. A good strategy is using one app for fashion (Afterpay), one for electronics (Affirm), and one for general use (Klarna or Zip). Track your total monthly BNPL obligations against your income to avoid overextension.

Final Thoughts

The buy now pay later landscape in 2026 offers far more options than FlexShopper alone. Klarna and Afterpay lead with interest-free Pay in 4 and massive retailer networks. Affirm provides the most transparent longer-term financing. Zip works anywhere Visa is accepted. Sezzle and Perpay actively build your credit with every payment. Fingerhut offers revolving credit for credit builders. Katapult matches FlexShopper as a lease-to-own alternative with no credit check. PayPal Pay in 4 keeps it simple for existing PayPal users. Splitit leverages your existing credit card. Sunbit covers service financing that other apps miss. Start with a 0% interest option (Afterpay or Klarna) for everyday purchases, and reserve lease-to-own platforms for essential items you need immediately. For more money management tools, explore our guides on budgeting, investing, health and fitness, and language learning.